Over the last few years, reported values and transaction prices of European football clubs have grown at an unprecedented rate. The differences between these data points continue to be stark, revealing a perplexing disconnect between the reported values and actual prices the clubs sell for. For instance, transaction prices for Manchester United F.C. and AC Milan S.p.A. were up to 100% higher than their most recent reported values at the time of each transaction. While it is common for notional “values” to differ from transaction “prices” (although they should not differ significantly), it is critical for a valuator to understand, explain, and attempt to reconcile these differences. The valuation approach and assumptions adopted in the derivation of the publicly reported values of many football clubs are often not available in the public domain, thus making it difficult to identify and understand the reasons for the large differences between the reported values and transaction prices.

The cultural importance of sports teams and the growing influx of capital in the sports industry mandates increased supervision and regulation to prevent financial malfeasance. While reported values can act as an indicator of industry trends and can be used in discussions amongst sports fans, these values may not be appropriate for reporting to regulators or sophisticated financial investors such as private and sovereign funds. Regulators and investors often seek greater clarity relating to the underlying assumptions and supporting evidence used in the reported value calculations before relying on such valuations to make decisions.

This article delves into the fascinating world of football club valuations, explores the methodologies used for publicly reported values, and identifies factors that contribute to the often-surprising gap between reported values and transaction prices. Further, it discusses potential reasons that could explain the discrepancy between the reported value and the transaction price for recent transactions involving Chelsea F.C., Manchester United, and AC Milan.

Valuation 101 — The What, Why, and How

The value of a sports team is determined based on future economic returns, which are influenced by factors such as the popularity of the sport and the team, the league’s competition structure, and team ownership structure.[1]

The value of any asset, such as a sports team, can be calculated for various purposes including structuring shareholder agreements, income tax reporting, estate planning, or a business transaction, such as mergers, acquisitions, or restructuring. Irrespective of the purpose, the value of an asset is determined under one (or more) of three approaches – income, market, and cost. A robust valuation generally triangulates value conclusions calculated under multiple approaches. For instance, a value determined using a discounted cash flow model, which is a popular method under the income approach, is often compared with conclusions under another approach, such as observed transactions or comparable asset multiples, which are popular methods under the market approach. The value conclusions can also be benchmarked against alternative indicators of value such as previous valuations, analyst reports, and industry commentary. We will discuss the technicalities of each valuation approach in a future article.

“Price”, which is the consideration paid in a negotiated open market transaction involving the purchase and sale of an asset, should not be conflated with “value”, which is determined in a notional market for hypothetical buyers and sellers. Notional value can differ from the open market transaction price of a subject asset for the reasons discussed below.

Existence of a special interest purchaser, who may desire to own a particular asset and is willing to pay more than others. Such purchasers would expect to enjoy incremental economic benefits post-acquisition and, hence would be willing to spend more to gain such synergistic advantages;

Emotional considerations such as the desire to own a particular sought-after asset;

Difference in knowledge and negotiating abilities between the buyer and the seller;

Legal or contractual restrictions that dictate the required actions of the buyer or the seller;

Distressed financial situation or a sale under duress, such as a bankruptcy auction; and,

The structure and consideration of the transaction, such as deferred payment terms, non-cash consideration, and earn-outs.

We discuss how these factors can help explain the gap between the reported values and transaction prices for recent transactions involving Chelsea, Manchester United, and AC Milan below.

Recent Valuations and Transactions involving top Football Clubs

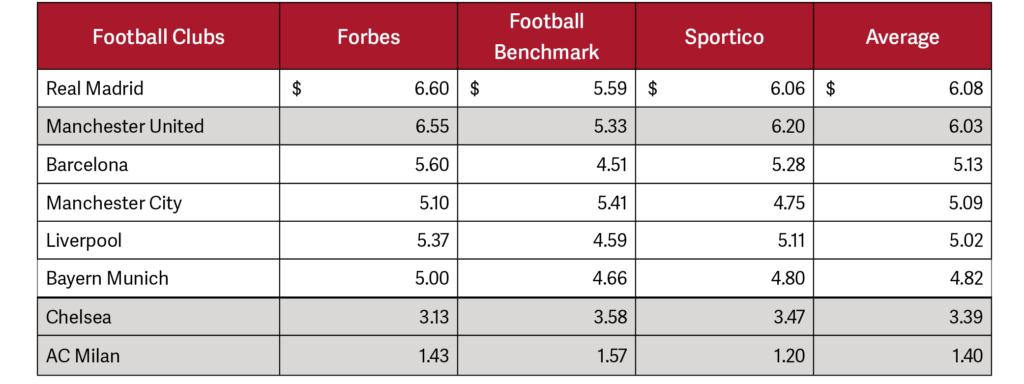

The values of the top-ranking football clubs are published annually by several organisations, such as Forbes, Football Benchmark, and Sportico. A summary of their reported values (in USD billions) for top football clubs in 2024 is provided below.

Figure 1: Reported values (in USD billions) for top football clubs in 2024[2]

On average, in 2024, Real Madrid is the highest-valued club at $6.08 billion, and Bayern Munich is the sixth highest at $4.82 billion.

All three publications used a market approach, specifically revenue multiples, as their valuation approach.[3] Under this approach, the valuator determines the enterprise value of a club based on its annual revenue and a multiplier. For example, if a club were to generate $10 million in annual revenue, and the assessed revenue multiple for valuing the club is 10x, the club’s value would be assessed at $100 million.

While all three publications reported the revenues for each club, the multiplier and the approach used to calculate the multiplier by each publication were not explained in detail. For instance, Sportico stated, “team-specific multipliers were based on multiple factors, including: historical sales, market (size, saturation and interest by prospective owners), strength of brand, on-field performance (historical and recent), terms of facility lease, debt burden and additional obligations, as well as expected future team and league economics”.[4] Football Benchmark noted that the revenue multiple method is “unsuitable for taking into account differences between football clubs”, and therefore, they have developed a proprietary algorithm “to reflect club-specific characteristics that influence clubs’ EV”.[5] Neither of the above-cited approaches provides any underlying data that can be independently reviewed or verified.

In addition, the difference between reported values and transaction prices for recent transactions continues to be stark. Looking at the top six football clubs based on reported values in 2024 (Figure 1), only Manchester United had partaken in a transaction in the past five years. In addition, Chelsea and AC Milan were also involved in transactions that were executed in 2022. Below, we analyse the reported values of Manchester United from 2016 to 2022, which was in and around the time of the reported transactions, and we discuss the potential reasons that could explain the discrepancies between the reported value and transaction price for Manchester United. We also provide commentary on Chelsea and AC Milan transactions.

Manchester United’s 2023 Transaction

On February 20, 2024, Sir Jim Ratcliffe acquired a 27.7% stake in Manchester United for $1.6 billion, which implied a total enterprise value of approximately $6 billion.[6] Sir Ratcliffe was given full control of the club’s football operations by the Glazer family.[7]

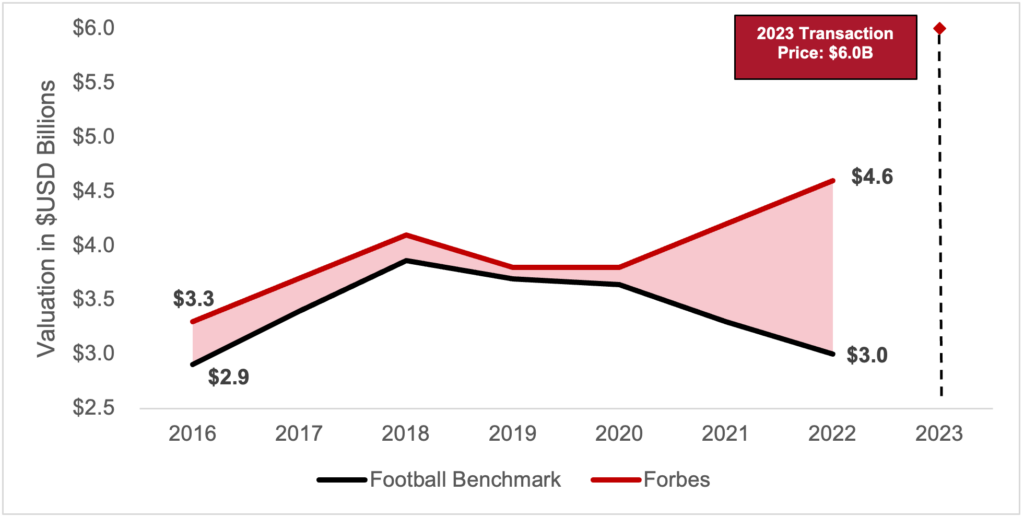

A chart depicting Manchester United’s reported values from 2016 to 2022 and the 2023 transaction price is presented below.

Figure 2: Manchester United Valuation and 2023 Transaction Price

As depicted in Figure 2, based on the Football Benchmark valuations, Manchester United’s reported value increased by $0.1 billion, or 3.2%, (from $2.9 billion to $3.0 billion), and based on the Forbes valuations, it increased by $1.3 billion, or 39.4% (from $3.3 billion to $4.6 billion) between 2016 and 2022. Further, the implied enterprise value of $6.0 billion based on the 2023 transaction is $1.4 billion to $3.0 billion (or 30% to 100%) higher than the 2022 reported values.

We considered the following factors that may have contributed to the difference between the reported values and the implied enterprise value of $6 billion based on the 2023 transaction with Sir Ratcliffe:

Manchester United is one of the most famous and successful football clubs in the world with numerous domestic and international titles, a loyal fanbase, a historic stadium (i.e., Old Trafford), and a globally recognised brand. All these factors made Manchester United a sought-after asset that would have a positive effect on price and could explain the discrepancy between the 2022 reported values and the transaction price.

The Glazer family’s relationship with Manchester United’s fans has been fragile since they acquired the club in 2005 for $942 million in a highly leveraged deal that loaded significant debt onto the club. After Sir Alex Ferguson, Manchester United’s legendary manager retired in 2013, the club’s on-field performances worsened which further damaged the relationship between the fans and the club hierarchy. Former players (e.g., Gary Neville[8]) and former executives (e.g., Michael Knighton[9]) criticised the Glazer family and the fans protested the ownership on several occasions.[10] The Glazer family was reportedly expecting to receive £10 billion (or $12.8 billion),[11] which was a significant premium over the reported value of $3.0 billion to $4.6 billion (Figure 2). However, faltering on-field performances of the club and the Glazer family’s fractured relationship with the fans precluded them from holding out for their desired valuation. While the Glazer family was not forced to sell the club, the club’s poor on-field performances, the fans’ ongoing protests and criticism against the ownership negatively affected their negotiating abilities.

Several global investors including private and sovereign funds enquired, but the Glazer family’s value expectations deterred the investors’ interests leaving only Sheikh Jassim of Qatar and Sir Ratcliffe as “serious bidders”.[12] Sheikh Jassim’s offer of £4.5 billion[13] ($5.75 billion) and Sir Ratcliffe’s acquisition at an implied enterprise value of $6.0 billion are above the reported value of $3.0 billion to $4.6 billion (Figure 2). Sheikh Jassim and Sir Ratcliffe are known to be Manchester United fans, making them special interest purchasers who desired to own the club and were willing to pay more than others.

As discussed above, Sir Ratcliffe acquired a minority or non-controlling stake of 27.7% in the club but was given full control of the club’s football operations by the Glazer family. Purchasers of a minority stake often discount the value reflecting their inability to control or influence the company’s operations or decisions. While obtaining full control over the club’s football operations would offset the discount, Sir Ratcliffe’s inability to control other commercial aspects of the club would still result in a lower pro-rata value in comparison to the pro-rata value on the acquisition of a majority (i.e., greater than 50%) stake.

Chelsea’s 2022 Transaction

In May 2022, Roman Abramovich sold Chelsea and related companies to an investment group led by Mr. Todd Boehly and Clearlake Capital for £2.5 billion (or $3.2 billion). The new owners also pledged to invest an additional £1.75 billion (or $2.2 billion) towards the development of the men’s and women’s teams and club’s infrastructure.[14] The buyers further agreed to retain their ownership in Chelsea for ten years, not issue any dividends, and adhere to limitations on debt.[15] As Mr. Abramovich was forced to sell the club due to sanctions imposed by the UK government and the sale proceeds were to be used for a charitable donation, Chelsea’s 2022 transaction is considered as a forced sale or distressed sale. These restrictions and circumstances would have had a negative effect in the 2022 transaction price.

Despite the distressed nature of the transaction, Chelsea’s 2022 transaction price of $3.2 billion (excluding the additional pledged investments of $2.2 billion)[16] is up to $0.9 billion[17] (or up to 37.7%)[18] higher than the 2021 reported values.[19] The sale of the club was concluded after a three-month process, during which they received 250 enquiries and 26 “strong bids”.[20] Mr. Abramovich was not interested in obtaining the highest possible consideration.[21] If Chelsea had been sold in the normal course of business, its transaction price could have been significantly higher because the club is based in London and has numerous domestic and international titles, a loyal fanbase, and a well-equipped stadium (i.e., Stamford Bridge)—all of these factors have a positive impact on its value.

AC Milan’s 2022 Transaction

In August 2022, RedBird Capital Partners acquired AC Milan from Elliott Management for $1.2 billion,[22] which is $0.6 billion[23] (or 100%)[24] higher than the 2021 reported values.[25] Elliot Management had acquired the club in 2018 after the club’s previous owner defaulted on a $300 million loan.[26] After acquiring the club in 2018, Elliott helped improve AC Milan’s on-field performances and cash flows by minimising payroll costs, which made AC Milan more attractive to potential purchasers.[27] Before the transaction closed in August 2022, AC Milan also won its first Serie A title in 11 years and qualified for the Champions League for the first time since 2014. RedBird Capital, who also own New York Yankees, stated that they would “leverage [their] global sports and media network, analytics expertise, track record in sports stadium developments and hospitality” and “explore opportunities together to broaden our fan reach and expand commercial opportunities globally” for AC Milan and Yankees.[28]All these factors would have had a positive effect on the 2022 transaction price and could explain the discrepancy between the 2021 reported values and the 2022 transaction price.

Conclusion

The valuation and sale of football clubs is a complex interplay of financial analysis, market dynamics, and the intangible allure of owning a sporting legacy. A robust valuation exercise includes an assessment of the expected future cash flows and the timing and risk associated with achieving such cash flows. Further, a valuator should test the reasonableness of their value conclusions by calculating values using other approaches such as market or cost approach and benchmarking their value conclusions against alternative indicators of value such as previous valuations, analyst reports, and industry commentary.

While the reported values based on the revenue multiple approach used by media houses such as Forbes, Football Benchmark, and Sportico provide a useful benchmark, they often fail to capture the unique value-driving aspects of a football club, such as its sporting performance, fan base, geographic location, and stadium characteristics, among others.

As the football industry continues to evolve, the gap between reported values and transaction prices may persist, reminding us that the value of these iconic clubs is not solely measured by their revenue but also by the passion they ignite and the history they represent.

Shalabh Gupta Associate Director | Toronto

Shalabh has provided financial analyses, economic advisory, forensic accounting, quantification of damages and other litigation support services to clients and their counsel for 10 years. He is a Chartered Accountant (CA), a Certified Fraud Examiner (CFE), and a Chartered Business Valuator (CBV).

Amran Nawaz Manager | Toronto

Amran has more than 8 years of experience in accounting and financial consulting, with specializations in the quantification of damages and valuations in the context of commercial and investment disputes. He is a Chartered Professional Accountant (CPA, CA) and a Chartered Business Valuator (CBV).

Andrew Costa Associate | Toronto

Andrew has provided audit, tax advisory and valuation services to multinational clients across several industries. He is a Chartered Professional Accountant (CPA) and has a Master of Accounting (MAcc) from the University of Waterloo.

[1]Secretariat, “Valuations of Sports Teams on the Rise: A Tale of Two Continents”, page 8, October 2023. [2]Forbes article, “World’s Most Valuable Soccer Teams – 2024”, May 23, 2024; Sportico article, “World’s 50 Most Valuable Soccer Clubs 2024 Ranking”, May 8, 2024 and Football Benchmark article, “The European Elite 2024: Football Clubs’ Valuation 9th Edition”. [3]Forbes article, “World’s Most Valuable Soccer Teams – 2024”, May 23, 2024; Sportico article, “World’s 50 Most Valuable Soccer Clubs 2024 Ranking”, May 8, 2024 and Football Benchmark article, “The European Elite 2024: Football Clubs’ Valuation 9th Edition”. [4]Sportico article, “World’s 50 Most Valuable Soccer Clubs 2024 Ranking”, May 8, 2024. [5]Football Benchmark article, “The European Elite 2024: Football Clubs’ Valuation 9th Edition”. [6] Calculated as: $6 billion = $1.6 billion / 27.7%. This is before any consideration of a potential minority discount incorporated into the purchase price, which would imply an even higher enterprise value for the entire club if one was considered. [7]INEOS Press Release, “Manchester United plc and Trawlers Ltd Announce the Successful Completion of Sir Jim Ratcliffe’s Minority Investment”, February 20, 2024; BBC article, “Manchester United: Sir Jim Ratcliffe’s £1.25bn deal for 27.7% stake is completed”, February 20, 2024 and Sportico article, “Manchester United Sells 25% Stake to Sir Jim Ratcliffe”, December 24, 2023. [8]Sky Sports article, “Gary Neville podcast: Desperate Glazers treating Manchester United like a toy… of course they’re going to sell”, September 4, 2023. [9]Sky News article, “Manchester United owners warned they have ‘run out of road’ and should sell up”, August 18, 2022. [10]Reuters article, “Who are the Glazers and why Manchester United fans don’t want them?”, November 23, 2022. [11]Daily Mail article, “EXCLUSIVE: Manchester United will be taken OFF the market by the Glazer family after bidders fail to reach their asking price in a huge blow to furious fans… as they hold out for £10BN for the club”, September 2, 2023. [12]Daily Mail article, “EXCLUSIVE: Manchester United will be taken OFF the market by the Glazer family after bidders fail to reach their asking price in a huge blow to furious fans… as they hold out for £10BN for the club”, September 2, 2023. [13]Sky Sports article, “Man Utd takeover: Qataris will not overpay as Glazers ask for £6bn”, March 10, 2023. [14]Reuters article, “Abramovich completes Chelsea sale to Boehly-Clearlake consortium”, May 30, 2022; and Chelsea FC Statement, “Club statement”, May 6, 2022. [15]The Straits Times article, “Football: ‘Not a big leap’ to say Chelsea’s value will double in 5 years: Raine Group’s Joe Ravitch”, September 28, 2022. [16]Reuters article, “Abramovich completes Chelsea sale to Boehly-Clearlake consortium”, May 30, 2022; and Chelsea FC Statement, “Club statement”, May 6, 2022. [17] Calculated as: $0.9 billion = $3.2 billion – $2.3 billion. [18] Calculated as: 37.7% = ($3.2 billion / $2.3 billion) -1. [19]Football Benchmark report, “Football Clubs’ Valuation: The European Elite 2021”, May 27, 2021. [20]Sky Sports article, “Chelsea owner Roman Abramovich sanctioned by UK Government“, March 12, 2022. [21]The Straits Times article, “Football: ‘Not a big leap’ to say Chelsea’s value will double in 5 years: Raine Group’s Joe Ravitch”, September 28, 2022. [22]The New York Times article, “Yankees Plant Flag in European Soccer (Again) With Stake in A.C. Milan”, August 31, 2022. [23] Calculated as: $0.6 billion = $1.2 billion – $0.6 billion. [24] Calculated as: 100% = ($1.2 billion / $0.6 billion) -1. [25]Football Benchmark report, “Football Clubs’ Valuation: The European Elite 2021”, May 27, 2021. [26]The New York Times article, “Yankees Plant Flag in European Soccer (Again) With Stake in A.C. Milan”, August 31, 2022. [27]The New York Times article, “Yankees Plant Flag in European Soccer (Again) With Stake in A.C. Milan”, August 31, 2022. [28]BBC article, “AC Milan: American investment firm RedBird buys Serie A club for £1bn”, August 31, 2022.

Tamika Tremaglio joined Emmy award-winning commentator Chris Hayes on his podcast “Why Is This Happening?,” for an in-depth conversation on the WNBA’s momentous CBA agreement and what it means for players, fans, investors, and the future of the league.

On February 24, 2026, the US Securities and Exchange Commission (SEC) released updates to its Enforcement Manual. In doing so, the SEC reaffirmed its commitment to “fairness, transparency, and efficiency” and highlighted key changes from the previous draft published in 2017.

The current conflict in the Middle East has been as disruptive commercially as it has been geopolitically. Many businesses operating in the region are suffering from a combination of sharp demand declines, blocked routes to market, surging input costs, and physical damage to assets.