Whether you are an economist, attorney, or simply interested in ideas at the intersection of law and economics, we are glad you found us. This publication includes insights from leading economists about recent developments in law and economics that may significantly impact the field.

This issue explores recent topics in the economics of AI-based discrimination, antitrust remedies in Big Tech, market definition in the cannabis industry, and the evolving antitrust allegations in college athletics.

In 2020, Epic, creator of the popular Fortnite game, filed a lawsuit against Google alleging that the company unlawfully maintained monopoly control over Android app distribution and in-app billing. Epic argued that Google engineered the Android ecosystem to steer app developers and users toward GPS, which required the use of GPB and allowed Google to collect a commission on transactions. The complaint further alleged that Google systematically undermined alternative app stores and payment options through contractual restrictions, technical design choices, and financial incentives. These practices, Epic alleged, preserved Google’s monopoly power, inflated commissions taken by Google on purchases through GPS/GPB, and reduced competition and innovation.[1] Notably, Epic did not seek monetary relief, stating: “Google’s conduct has caused and continues to cause Epic financial harm, but Epic is not bringing this case to recover these damages; Epic is not seeking any monetary relief, but rather only an order enjoining Google from continuing to impose its anti-competitive conduct on the Android ecosystem.”[2]

After a multi-week trial in late 2023, a federal jury unanimously found Google liable for violating federal and state antitrust laws by monopolizing Android app distribution and in-app payments and unlawfully tying GPS to GPB.[3] Following the verdict, U.S. District Judge James Donato entered a permanent injunction mandating changes to GPS aimed at fostering competition. This included, among other things, requiring that Google allow alternative app stores to be available for download on GPS, allow alternative app stores to access the GPS app catalogue, and allow app developers to use payment options other than GPB.[4] Google appealed, but, on July 31, 2025, the Ninth Circuit unanimously upheld both the jury verdict and the permanent injunction.[5] Google continued to appeal the decision as the deadline to implement elements of the permanent injunction approached, requesting a partial stay from the Supreme Court, which was declined in October 2025.[6]

The Proposed Settlement

The next month, in November 2025, Epic and Google announced a settlement and proposed several modifications to the injunction. Among the changes, the proposal would allow Google to deny alternative app stores access to the GPS app catalog and continue to exclude the alternative app stores from distribution through GPS, instead only allowing that distribution through “sideloading” (installation outside of GPS). Additionally, unlike the original injunction, which did not have requirements related to commission rates, Google agreed to cap the commission rate on GPS. Despite the proposed capped fees, Google and Epic’s terms would modify the injunction’s requirement to break the GPS/GPB tie, instead allowing developers to bypass GPB but still be charged (capped) services fees by Google on those transactions.[7]

Judicial and Third-Party Scrutiny

The proposed modifications, which generally limited the reach of the injunction, were met with skepticism and concern. Injunctions are not typically modified unless, among other potential reasons, there has been a significant change in circumstance. Judge Donato was not convinced that such a change was evident, noting: “The only changed circumstance that I can see right now is Epic and Google — two mortal enemies who pounded each other relentlessly in this courtroom for many years — are suddenly BFFs.”[8] Judge Donato further questioned if the proposal would “prov[e] an adequate remedy for Google’s wrongdoing.”[9]

This scrutiny has raised the possibility that the settlement could be rejected or require significant modifications. In a December 2025 order, Judge Donato scheduled an evidentiary hearing for January 2026 to discuss the proposed modifications.[10] The Court also announced that it was appointing an economist unaffiliated with either party, Prof. Nancy L. Rose,[11] to “assist the Court in evaluating whether the joint request to modify the injunction [. . .] is consistent with the jury verdict and the public interest in free and unfettered competition.”[12] Later, in a text order prior to the evidentiary hearing, Judge Donato noted that the signatories for the proposed settlement from each of the parties would be expected to testify.[13]

The proposed modifications to the injunction also drew several amicus briefs from outside parties that underscore the public-interest dimension of this case. The first of these briefs was filed by a group of “scholars of economics and law”, which included Paul Heidhues, Gene Kimmelman, Giorgio Monti, Fiona Scott Morton, Rupprecht Podszun, and Monika Schnitzer.[14] The amici expressed concern that the suggested modifications to the injunction would effectively make Google’s monopoly a Google-Epic shared duopoly, continuing to keep out other potential rivals and stifle competition.[15]

Next, amicus briefs from Microsoft and the FTC were also filed.[16] These, too, noted concerns with the economic effects of the proposed modifications to the injunction. Microsoft amici noted that the modifications would “effectively allow Google to restore [its] unlawful tie.”[17] The FTC amici raised concern that “private parties such as Google and Epic may barter away the public interest embedded in the court’s injunction for private gain.”[18] The commission “urge[d] the Court to consider the extent to which privately beneficial terms in the comprehensive settlement could have induced Epic to accept modifications that would not necessarily serve the public interest in competition.”[19]

Partnerships, Incentives, and Competition

At the January evidentiary hearing, Judge Donato indicated that it would be unlikely that he would grant the parties’ modifications.[20] One element that heightened concern was the disclosure of a commercial partnership between Epic and Google that surfaced during the proceedings.[21] Epic agreed to pay Google $800 million over six years for collaboration involving Epic’s Unreal Engine and joint marketing efforts. Epic CEO Tim Sweeney noted that this would give Epic a chance to expand its market reach, when asked by Judge Donato what Epic was “getting out of this” part of the deal.[22] Judge Donato questioned whether this agreement may be influencing Epic’s and Google’s incentives regarding the proposed modifications.[23]

Although this partnership does not, by itself, determine the welfare effects of relief measures, it amplifies judicial demand for clear economic justification for the proposed modifications. Indeed, at the January 2026 hearing, Judge Donato called on Prof. Douglas Bernheim,[24] who served as Epic’s economic expert during the course of the litigation, questioning if Prof. Bernheim agreed with the modified injunction.[25] While Prof. Bernheim stated that the modified injunction was “a better model for achieving sustainable competition,” Judge Donato was not convinced, noting his concern that the deal “put Epic and Epic alone, unlike any other developer or app provider, in a special relationship, vis-à-vis Google.”[26]

The skepticism of the Court and amicus submissions reinforce that this case is not just a private dispute between two parties, and thus, the proposed injunction is not only to benefit a given party. Instead, the case and resulting injunction are focused on benefiting competition, not just one competitor. Indeed, as discussed above, even in Epic’s complaint, it noted the importance of “enjoining Google from continuing to impose its anti-competitive conduct on the Android ecosystem,” rather than only making Epic financially whole. As such, the Court must consider these proposed modifications through an economic lens that encompasses the entirety of the market.

Economic Implications for Platform Competition

From an economic perspective, the key issue is whether the proposed modifications would meaningfully promote competition in the Android app ecosystem or instead preserve Google’s market power, albeit in a modified form. The original injunction sought to reduce entry barriers, weaken Google’s network-effect advantages, and enable rival app stores and payment systems to reach viable scale, allowing meaningful competition in the market. By contrast, the proposed modifications replace structural openness with capped pricing and limited access. Economic theory and antitrust literature suggest that regulatory price caps (or similar constraints) can often be a poor substitute for actual competitive contestability. Rather than fostering genuine competition, such regulation can lead to an unlawful monopoly converting into a regulated monopoly or narrow duopoly.[27] Restricting alternative app stores to sideloading and allowing Google to impose fees even when GPB is bypassed may threaten to recreate the bottlenecks and tying dynamics that the jury found unlawful.

The settlement has also raised concerns about asymmetric benefits. Remedies that primarily advantage a single large developer (here, Epic) may increase that developer’s private surplus without improving outcomes for the rest of the market (e.g., smaller developers, consumers). This may also continue to deter market entry by signaling that individualized deals with the dominant platform (here, Google) are required in order to successfully compete. Antitrust remedies must be judged by their economic effects on market wide incentives that seek to encourage entry, multi-homing, and/or competition on price, quality, and innovation. Viewed in this light, the skepticism of the Court and amici reflects a concern that the proposed modifications trade a market-wide competition-enhancing remedy for a privately efficient settlement, undermining the broader public-interest goals of antitrust enforcement.

This may serve as a test case for digital platform remedies in U.S. antitrust enforcement, where antitrust scrutiny and private litigation continue to focus. With settlement approval looking less likely, Epic v. Google continues to be a case to watch in 2026. Epic v. Google has expanded the role of economic analysis in antitrust litigation and could shape how courts assess competition and remedies in platform markets for years to come.

Note: Since this article was written and finalized, Google and Epic have filed amended proposed modifications to the Court’s injunction. On March 4, 2026, parties submitted a revised set of modifications, claiming that it “hews much more closely to the Existing Injunction than did the parties’ previous proposal and is designed to address the concerns raised at the January 22, 2026 hearing.” (Dkt. 1179) The status of the settlement, the injunction, and the newly proposed modifications remains ongoing. These developments underscore the importance of the economic considerations underlying remedies in antitrust matters, as discussed in this article, and reflect the parties’ continued efforts to craft a resolution that addresses both the Court’s concerns in the market, rather than only between parties.

[1] In re: Google Play Store Antitrust Litigation, Dkt 1.

Following Epic’s filing, several other cases were filed by a class of GPS consumers, a class of app developers, a coalition of state attorneys general, and the Match Group (owner of several dating apps, such as Tinder). These separate filings were consolidated into In re: Google Play Store Antitrust Litigation.

[2] In re: Google Play Store Antitrust Litigation, Dkt 1. (Emphasis in original.)

[3] Dkt 866

[4] Dkt 1017

[5] https://www.law360.com/articles/2305370

[6] https://www.supremecourt.gov/orders/courtorders/100625zr_3fbh.pdf

[7] Dkt 760-1

[8] https://www.law360.com/articles/2408618

[9] https://www.law360.com/articles/2408618

[10] Dkt 1130

[11] Nancy L. Rose is the Charles P. Kindleberger Professor of Applied Economics, Massachusetts Institute of Technology Department of Economics.

[12] Dkt 1131

[13] Dkt 1146

[14] Dkt 1156-1

Paul Heidhues is Professor of Behavioral and Competition Economics, Düsseldorf Institute for Competition Economics (DICE), Heinrich-Heine University of Düsseldorf.

Gene Kimmelman is Senior Policy Fellow, Tobin Center for Economic Policy at Yale University and Research Fellow, Mossavar-Rahmani Center for Business & Government at the John F. Kennedy School of Government at Harvard University.

Giorgio Monti is Professor of Competition Law at Tilburg Law Chol, Tilburg Law and Economics Center, and Research Fellow, Centre on Regulation in Europe.

Fiona Scott Morton is the Theodore Nierenberg Professor of Economics at the Yale University School of Management, and former Deputy Assistant Attorney General for Economic Analysis (Chief Economist) at the Antitrust Division of the U.S. Department of Justice.

Rupprecht Podszun is Chair of Civil Law, German and European Competition Law at Heinrich Heine University of Düsseldorf, Director of the Institute of Antitrust.

Monika Schnitzer is Professor of Economics, Ludwig-Maximilians-University Munich.

[15] Dkt 1156-1

[16] Dkt 1159-1

Dkt 1163-2

[17] Dkt 1159-1

[18] Dkt 1163-2

[19] Dkt 1163-2

[20] https://www.law360.com/articles/2433248

[21] https://www.law360.com/articles/2433248

[22] https://www.law360.com/articles/2433248

[23] https://www.law360.com/articles/2433248

[24] Douglas Bernheim is the Edward Ames Edmonds Professor of Economics, Stanford University Department of Economics.

[25] https://www.law360.com/articles/2433248

[26] https://www.law360.com/articles/2433248

[27] Hovenkamp, Herbert (2021). “Antitrust and Platform Monopoly,” The Yale Law Journal 130(7):1952–2005.

This framework was directly challenged in O’Bannon v. NCAA (2015), which focused on the NCAA’s prohibition on compensating athletes for the use of their names, images, and likenesses (NIL), especially in video games and broadcasts. The Ninth Circuit ruled that while the NCAA could maintain some limits tied to amateurism, its complete ban on NIL-related compensation violated antitrust law. On July 1, 2021, a wave of state legislation and new NCAA policies allowed college athletes to begin signing endorsement deals and earn revenue on their NIL.

Another consequential recent ruling came in NCAA v. Alston (2021), where the Supreme Court unanimously affirmed that NCAA limits on education-related benefits—such as scholarships for graduate school, tutoring, or laptops—were unlawful restraints of trade. Notably, the court rejected the NCAA’s broad claims that amateurism justified deference under antitrust law and openly questioned the legality of nearly all NCAA compensation restrictions. While Alston technically addressed only education-related benefits, its reasoning signaled broad skepticism toward the NCAA’s business model.

The House v. NCAA settlement was the most recent antitrust resolution that significantly changed how college athletes at certain institutions may be compensated.[1] Approved in 2025, it resolved multiple lawsuits alleging that the NCAA had unlawfully restricted athlete pay in violation of federal antitrust law. As part of the settlement, schools are now permitted to share athletic revenue directly with athletes, subject to annual caps. While the settlement does not classify athletes as employees, it effectively dismantles the NCAA’s traditional amateurism model and marks a structural shift toward a revenue-sharing system in college sports.

Despite implementing these significant changes, the NCAA cannot reasonably expect the end of legal challenges on antitrust grounds. Recent cases suggest that the next battleground may revolve around the NCAA’s eligibility rules.[2] As it currently stands, the NCAA provides student athletes with four years of athletic eligibility within a five-year period. According to the NCAA, this five-year clock begins once the athlete enrolls at any collegiate institution, regardless of whether its athletic programs operate within the NCAA. The clock does not reset when the athlete transfers to a different school.

Under the prior regime—before revenue-sharing and NIL agreements—the NCAA’s eligibility requirements were relatively innocuous, from an economic perspective. Although many athletes received valuable in-kind benefits related to tuition and living expenses, participation in collegiate sports did not involve direct monetary compensation. As a result, for many athletes, the economic opportunities available outside of college were strictly superior to those available within it. This disparity was especially pronounced for elite athletes in highly lucrative professional sports, such as football and men’s basketball. For these athletes, the requirement that they compete without monetary pay in college—often due to age-based professional league restrictions—was widely understood as an economic sacrifice.[3]

However, under the current regime, and for a select group of individual athletes, the economic returns to remaining in college may now far exceed the income available outside of the NCAA. This dynamic is particularly pronounced for athletes in sports without highly paid professional leagues, such as gymnastics. As an extreme example, Louisiana State University (LSU) gymnast Olivia Dunne reportedly earned an estimated $4.1 million in endorsement deals during her fifth year of eligibility.[4] Whether that level of brand value can be sustained beyond the college sports ecosystem remains to be seen.

Moreover, women’s college basketball players may now earn substantially more through NIL arrangements than they would as professionals in the Women’s National Basketball Association (WNBA). As of June 2025, top NIL earners in women’s college basketball reportedly secured deals ranging from roughly $300,000 to $1.5 million, while the salary for a first-round WNBA draft pick begins at approximately $75,000.[5] The highest paid WNBA player in 2025 commanded an annual average salary of $252,450.[6] For players who fear that their marketability may diminish upon leaving a prominent college program, these disparities create a strong economic incentive to remain in college for an additional year.

Importantly, this incentive is not limited to athletes without lucrative professional alternatives. Even in sports such as football and men’s basketball, the opportunity cost of remaining in college for an additional year has fallen substantially. With the availability of NIL income and revenue-sharing arrangements, athletes now forgo less by staying in school an extra season to develop their skills and potentially improve their draft position. Indeed, a recent study of player’s decisions to enter the NBA draft between 2019–2024 finds that, following the liberalization of NIL rules, more men’s college basketball players choose to use their remaining collegiate eligibility.[7]

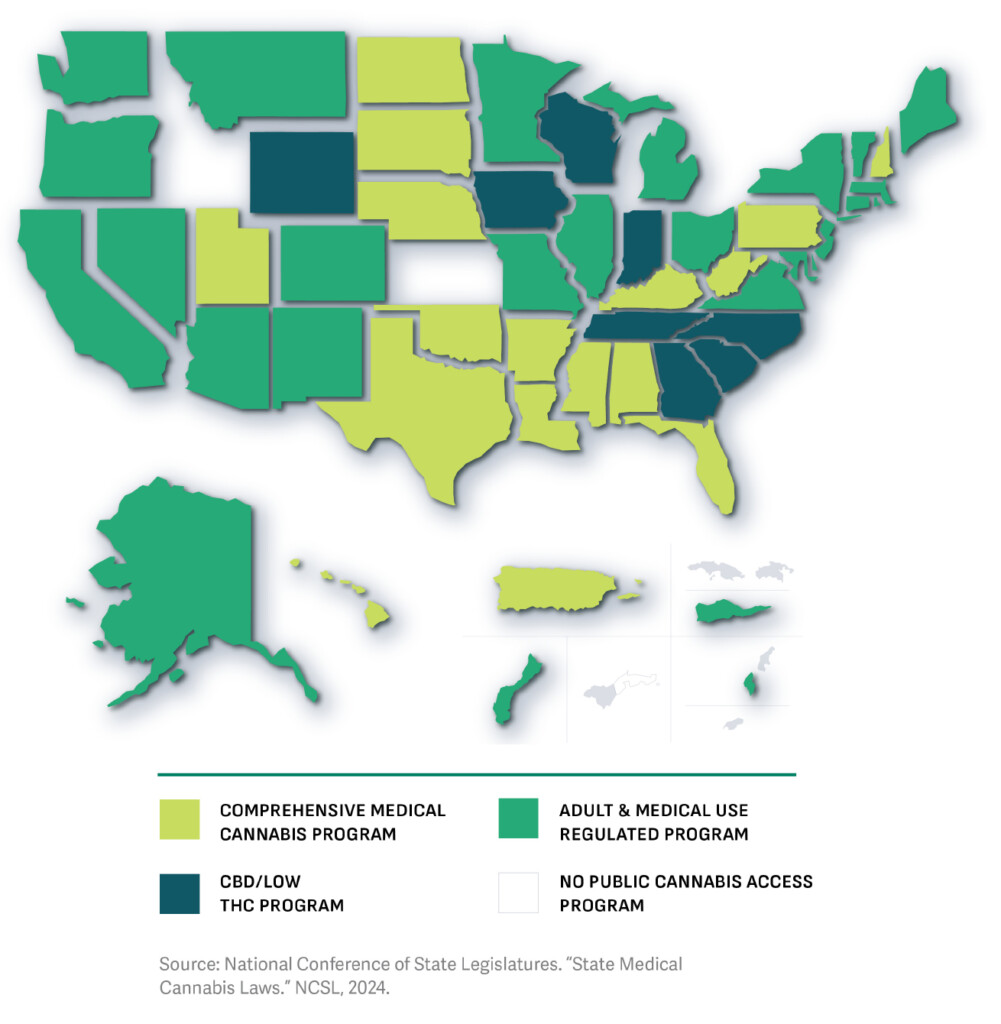

The state of competition in the U.S. cannabis industry is uniquely complex due to the interplay between federal prohibition[1] and state-level legalization.[2] In states that have legalized medical or recreational use of cannabis, the sector has expanded rapidly.[3] This has created a patchwork of local markets with barriers to interstate commerce, that to some extent insulates regional operators from the broader competitive pressures. The map herein illustrates how state regulations differ across the country. Although the FTC and DOJ retain jurisdiction to apply federal competition law, the continued federal illegality of cannabis under the Controlled Substances Act has created institutional uncertainty regarding the scope and propriety of federal engagement. In practice, most competition disputes in the sector have been addressed by state attorneys general and private litigants.

These diverse state-level policies have, to some extent, shaped the structure of the modern U.S. cannabis industry,[4] which is best understood as a vertically structured supply chain rather than a single unified market. At the upstream level are cultivators that grow cannabis plants and manufacturers that process raw cannabis into derivative products such as concentrates, edibles, tinctures, and infused goods. Within this level, firms differentiate themselves through branding, potency, and product format.[5] Downstream are distributors (in some states) and retail dispensaries that sell directly to consumers. Because regulation varies by jurisdiction, some firms operate across multiple stages while others are restricted to a single level.

The cannabis industry continues to operate in an uncertain regulatory landscape, where antitrust enforcement is highly fragmented.

Potential antitrust issues can arise at every level of the U.S. cannabis industry under the current market structure. Horizontal concerns may occur among growers, manufacturers, or retailers competing within the same tier. In addition, vertical relationships—such as supply agreements, exclusivity provisions, and integration mandates—create potential vertical restraint issues linking different levels of the industry. Regulatory features including licensing caps and vertical integration requirements can amplify these concerns by limiting entry and altering competitive incentives.[6],[7]

Regulators and policymakers have increasingly expressed concern regarding state cannabis regulatory frameworks,[8] in particular to the increased consolidation among MSOs.[9] Vertical integration requirements in some states—where licensees must control multiple stages of the supply chain—can limit competition by favoring larger, better-capitalized companies.[10] Additionally, licensing caps and residency requirements often restrict the entry of new competitors, which can lead to oligopolistic market structures. Courts have increasingly entertained constitutional and competition-related challenges to state protectionist rules, such as residency requirements for cannabis licenses.[11] These dynamics may unintentionally foster anti-competitive environments that could harm consumers and small businesses.

Similar allegations regarding bias embedded in AI-driven decisions have been made in the insurance industry about wrongful coverage denials and discrimination in underwriting and claims processing. At the core of these cases is whether reliance on AI-based decision making constitutes a common policy sufficient to render putative class members similarly situated for purposes of class certification.

AI Decision-Making and Discrimination Risk

Organizations often make decisions that impact prospective and current employees or customers. A subject of concern that may lead to litigation is the disparate treatment of members of a protected class, such as age, race, or gender, in decisions, including admissions, underwriting, coverage, hiring, promotion, compensation and termination. Reliance on AI-based algorithmic decision-making is often intended to reduce subjective bias. Recent litigation, however, underscores that AI tools may not be bias-free and may incorporate, and even potentially accentuate, biases associated with the historical data on which these models are trained.

In Mobley v. Workday, Inc., the plaintiff claims that Workday’s AI-based screening algorithm disproportionately disqualified applicants over 40 years old from employment opportunities. Workday operates a two-sided platform that allows job candidates to submit applications and employers to collect, process, and screen them. The plaintiff alleges that the algorithms were trained only on incumbent employee data, which resulted in a homogeneous workforce that was not representative of the applicant pool and was discriminatory against applicants over 40. In granting preliminary class certification, Judge Lin identified Workday’s algorithmic decision-making tools as discriminatorily scoring applications based on age. Judge Lin further concluded that members of the proposed class were similarly situated because the basis for the denial of employment was that applicants were subject to the same common policy—in this case, the same algorithmic decision-making tools, regardless of any disparate impact across claimants. Judge Lin, however, explained that this preliminary decision did not preclude the possibility that AI recommendations are in fact the result of individual employer preferences and recommendations, in which case an AI-based common policy would not be identifiable.

Why AI Systems May Not Constitute a Common Policy

This qualification highlights a critical question: are outcomes of interest attributable to individual human actions or common AI rules? Several factors suggest that AI-based hiring systems might not always result in uniform policies. First, even though predictive statistical models and algorithms provide information about objective metrics of performance, in practice, these objective metrics are often supplemented with human input to assess some subjective aspects of applications, such as cultural fit or interpersonal skills. In such cases, final decisions may not conform to a common policy and are better understood as the result of both model-driven analysis and a layer of human oversight involving individualized evaluation of a person’s attributes. This will ultimately depend on how these screening systems are used. For example, if a recommendation system automatically rejects individuals above a certain age, with no human review, those applicants may plausibly be subject to a common policy.

Second, AI-based decision making may involve employer-specific customization, with parameters defined on a case-by-case basis, which may explain why the AI system does not operate in a unified way. For instance, screening models may be trained on employ-er-specific historical hiring data and tailored to each employer’s criteria for a successful applicant. In such circumstances, disparate outcome analyses may not be susceptible to common proof.

Third, AI models evolve over time, which runs counter to the existence of a uniform policy and may be more consistent with a non-static policy. A defining characteristic of AI models is their reliance on feedback loops as a basis to learn and improve decision-making over time. Performance data provides a basis for re-training and refining algorithmic decision-making. Feedback loops, however, do not necessarily self-correct. For example, if an algorithm is trained on historical data showing that a company often hires candidates under 40 years old, the algorithm may initially learn that bias and amplify it with successive self-reinforcing recommendations in favor of younger hirings.

The court concluded in this case, which plaintiff Students for Fair Admissions has appealed, that relying solely on a subset of the information that USNA considered in its holistic admissions reviews likely leads to overstated estimates of the impact of race and ethnicity on USNA’s admissions decisions. The ruling explores the bounds on the probative value of statistical evidence of discrimination. The remainder of this article draws lessons on what those bounds are from which econometric arguments did and did not appeal to the judge.

An oversimplified regression model of admissions cannot reliably estimate the contribution of race to admissions decisions

Multiple regression analysis is a statistical technique used to quantify the relationship between an outcome of interest and several explanatory variables. In the context of race-based discrimination litigation, the outcome of interest might be college admissions, loan or hiring decisions, or quality of medical care. By including race alongside sufficient other relevant factors, researchers can estimate the independent effect of race on the outcome of interest. In SFFA v. USNA, the key statistical question was whether the regression model provided by SFFA’s expert included enough other relevant factors to isolate the effects of race and ethnicity on the Naval Academy’s admissions decisions from the effects of variables such as socioeconomic background.

USNA acknowledged considering race and ethnicity as one of many factors in its holistic review of applicants’ files. SFFA’s expert attempted to quantify the impact of race and ethnicity on admissions decisions using a logit regression model that explains the probability of admission with several factors, including race and ethnicity. Secretariat Managing Director Dr. Stuart Gurrea, serving as a testifying expert for USNA, argued that this model oversimplified the complex admissions process and produced unreliable estimates of the impact of race and ethnicity. The court agreed with this assessment, finding that SFFA’s model failed to account for many other factors the Academy considered in its admissions process.

Difference-in-Differences (DiD) analysis has been a popular method in econometrics for estimating causal effects and is often employed in antitrust litigation. The essence of DiD lies in comparing the changes in outcome variables of interest (e.g., price) over time between a group that is exposed to the alleged anticompetitive conduct and a control group that is not (e.g., comparing different groups of consumers, different firms, or different geographic regions). It gets its name “difference-in-differences” because it essentially combines two types of variation—the first from a before-and-after analysis and the second from comparing an affected and an unaffected group.

The key advantage of DiD is its ability to control for time-invariant unobservable factors that may influence the outcome of interest. By differencing out the common time trends between the groups that are and are not affected by the anticompetitive conduct (i.e., “treatment” and “control” groups), DiD isolates the treatment effect by focusing on the differential changes in outcomes that occur after the introduction of the treatment. The DiD methodology has been implemented in antitrust analyses in various settings.2 In merger analysis, for example, DiD has often been implemented to estimate retroactively the impact of past consolidations to inform future policy.3

Despite its strengths, DiD is not immune to potential biases. Choosing the right quantitative tool, such as DiD, in an antitrust setting involves careful consideration of various factors to ensure the validity of the causal inference. Under the Daubert Standard,4 it is important for an expert to demonstrate the adequacy of a chosen tool, such as regression, and the appropriateness of a chosen research design.5 Since biases in the canonical DiD may arise from the violation of distinct conditions, there is no single recipe solution, and experts need to carefully analyze the case in question.6

There may be situations where a simple pre– and post-treatment formulation is not enough to capture the dynamics. For example, a company’s pricing policy may go into effect in distinct regions at different times as opposed to being simultaneously launched. There might be a need to study the effect of successive acquisitions by the same company in different markets. A firm may choose to implement a new policy to distinct groups of stakeholders at different times. As in these examples, the resulting bias of the estimates obtained by applying the standard DiD will be particularly problematic when there is heterogeneity in the treatment effect over time. However, there have been a few methodological alternatives proposed in the literature,7 some of which have been used in litigation.8 One could, for example, use a matching algorithm in each period to pick the best control group (where only those units that are untreated in that period are candidates),9 and once the control groups are selected, proceed as usual.

DiD also requires the treatment and control groups to have similar trends over time in the absence of the alleged anticompetitive conduct. In practice, this means that, absent a merger, and with everything else held constant, prices in markets where both merging parties are present (treatment group) and markets where at least one of them is not (control group) would have trended in a similar fashion. A violation of this assumption need not be the end of DiD analysis, but it does require one to adjust one’s specifications, as the regression will no longer produce consistent estimates merely by incorporating time-independent variables. If this violation of the parallel trends happens due to an observable factor, it is possible to extend the assumption by conditioning on variables that are observable pre-treatment.10

Most DiD literature imposes the requirement that potential outcomes of a unit are unaffected by the treatment assignment of other units – in other words, the variable of interest for that unit only depends on whether that unit and that unit only has been exposed to the anticompetitive conduct, which guarantees independence and essentially rules out any spillover effects. In our earlier example, customers can only be affected if the conduct has occurred in their market, but ought to be unaffected otherwise, all else held constant. However, it is possible that, if individuals are connected by a network, there may be spillover effects. A growing literature has already accounted for some extensions of the general framework that account for these network effects,11 but there will likely be many more developments in this area, which may particularly impact how antitrust litigation views competition when platforms are involved.12 For example, one might consider how changes in Gen AI policy that are applicable only to European markets start affecting the way companies conduct business in the United States, despite the absence of any such policy change in the United States.

In conclusion, DiD remains a valuable tool for estimating causal effects, offering a quasi-experimental approach to understanding and estimating the economic implications of alleged anticompetitive practices. Recent econometric developments have significantly enhanced the method’s applicability, addressing concerns related to control group selection, unobserved heterogeneity, and group trends. By incorporating appropriate adjustments to their DiD specifications, antitrust experts can improve the robustness of their estimates, ensuring that antitrust enforcement remains grounded in sound economic principles and evidence-based reasoning. As econometrics continues to evolve, it is paramount that practitioners stay up to date with state-of-the-art quantitative techniques, allowing DiD analysis to contribute to more accurate and reliable causal inference in antitrust cases.

1See, for example, U.S. Department of Justice & Federal Trade Commission, Merger Guidelines, (2023) (henceforth Merger Guidelines), §1 & ft. 7.

2See, for example, Messner v. Northshore University HealthSystem, 669 F.3d 802 (United States Court of Appeals, 7th Cir. 2012) concluded that experts can use “difference-in-differences methodology to estimate [] anti-trust impact”.; In re AMR Corporation, 625 B.R. 215 (United States Bankruptcy Court, S.D.N.Y. 2021); Mr. Dee’s Inc. v. Inmar Inc., No. 1:19cv141, (United States District Court, M.D. North Carolina. 2021); In re Dealer Management Systems Antitrust Litig., 581 F. Supp. 3d 1029 (Dist. Court, ND Illinois. 2022); Tevra Brands LLC v. Bayer Healthcare LLC, No. 19-cv-04312-BLF, (N.D. Cal. Apr. 15, 2024).

3See, for example, Joseph Farrell et al. (2009), Economics at the FTC: Retrospective Merger Analysis with a Focus on Hospitals, 35 (4 – Special Issue: Antitrust and Regulatory Review) Review of Industrial Organization, 369-385 (2009); Graeme Hunter et al., Merger Retrospective Studies: A Review, 23 (1) Antitrust, pp. 34-41 (2008); Dennis Carlton et al., Are legacy airline mergers pro- or anti-competitive? Evidence from recent U.S. airline mergers, 62 International Journal of Industrial Organization, pp. 58-95 (2019).

4The Daubert Standard was established in the U.S. Supreme Court case Daubert v. Merrell Dow Pharmaceuticals Inc., 509 U.S. 579 (1993), and provides a systematic framework for a trial court judge to assess the reliability and relevance of expert witness testimony before it is presented to a jury.

5See, for example, Mia. Prods. & Chem. Co. v. Olin Corp., No. 1:19-CV-00385 EAW (W.D.N.Y. Dec. 28, 2023), where regression model was classified as “not methodologically sound, for multiple reasons”, including endogeneity and misclassifying data; Reed Constr. Data Inc. v. McGraw-Hill Cos., 49 F. Supp. 3d 385 (S.D.N.Y. 2014) where Daubert motion to exclude expert’s regression analysis was granted due to significant failures, including faulty model design, omitted variable bias, and multicollinearity.

6There are some excellent papers that summarize the recent advances in the literature. See, notably, Jonathan Roth et al., What’s trending in difference-in-differences? A synthesis of the recent econometrics literature, 235(2) Journal of Econometrics, 2218 (2023) (henceforth “Roth et al. (2023)”). Moreover, Baker, Andrew, et al. “Difference-in-differences designs: A practitioner’s guide.” arXiv preprint arXiv:2503.13323 (2025) offers a comprehensive and accessible overview of the theory, assumptions, implementation, and recent methodological advances in DiD designs, with a focus on practical applications in empirical research.

7See, for example, Andrew Goodman-Bacon, Difference-in-differences with variation in treatment timing, 225(2) Journal of Econometrics, 254, (2021); Brantley Callaway & Pedro H.C. Sant’Anna, Difference-in-Differences with multiple time periods, 225(2) Journal of Econometrics, 200, (2021) (henceforth “Callaway & Sant’Anna (2021)”); Kirill Borusyak, Xavier Jaravel, & Jann, Spiess, Revisiting Event Study Designs: Robust and Efficient Estimation, arXiv preprint arXiv:2108.12419 (2021)

8See, for example, Ryan LLC v. Federal Trade Commission, Docket No. 3:24-cv-00986 (N.D. Tex. Apr 23, 2024), ECF 210.

9This has been a gross overview of the methods described in Callaway & Sant’Anna (2021), supra note 7.

10There are several ways that the literature has proposed to operationalize the implementation of conditional parallel trends, such as: i) regression adjustment which essentially entails including additional observable and measurable characteristics (these observable and measurable characteristics from each unit can be called covariates) in the regression model to control for potential confounding factors, and allows for a more nuanced analysis of the variable of interest (inference with this approach can become complicated with a fixed number of matches); ii) inverse probability weighting which will explicitly model the probability that each unit belongs to the treated/control given some covariates (see Alberto Abadie, Semiparametric Difference-in-Differences Estimators, 72(1) The Review of Economic Studies, 1 (2005) for original derivation); iii) doubly-robust estimators which combines both methods previously mentioned (See Pedro HC Sant’Anna & Jun Zhao, Doubly robust difference-in-differences estimators, 219(1) Journal of Econometrics, 101 (2020)).

11See, for example, Kyle Butts, JUE Insight: Difference-in-differences with geocoded microdata, 133 Journal of Urban Economics 103493 (2023); Martin Huber & Andreas Steinmayr, A framework for separating individual-level treatment effects from spillover effects, 39(2) Journal of Business & Economic Statistics 422 (2021).

12There is a growing concern by competition agencies with respect to potential spillover effects and the need to account for these in antitrust investigation. See, for example, Merger Guidelines, supra note 1, §2.9.: “Network effects occur when platform participants contribute to the value of the platform for other participants and the operator. The value for groups of participants on one side may depend on the number of participants either on the same side (direct network effects) or on the other side(s) (indirect network effects).”

However, more generally, MFNs can also apply to vertical agreements between suppliers and buyers, where, for example, a seller promises a buyer that the buyer will always be offered the lowest price offered by the seller.2 While the exact details of these provisions differ by contract, parties, and setting, MFN clauses generally require that one party to the transaction not offer better contractual terms to any other party.3

With the rise of technical platforms, an entity that facilitates interaction/transactions between one or more groups of users (e.g., consumers and suppliers),4 MFN clauses have made their way into agreements between platforms and platform participants. These are known as platform MFN (PMFN) clauses. Generally, PMFN clauses are imposed by the platforms on the sellers/suppliers and prohibit sellers/suppliers from offering buyers/consumers products or services more favorably (e.g. lower price, better offering) on any other platform or distribution channel.5 PMFNs can vary based on the reach of the provision. A “narrow PMFN” prevents a seller/supplier from offering more favorable products or services using its own distribution channel, while a “wide PMFN” extends this prohibition to all other platforms, in addition to the seller’s/supplier’s own distribution channel.6

A key difference between classic MFNs and PMFNs is that the platform is not purchasing a service or good from a seller/supplier; rather, the platform is paid a cut from sales that occur on the platform. Thus, rather than a traditional MFN restricting the price at which a supplier can sell to a buyer’s competitors, a PMFN puts a floor on the price the participants on the seller-/supplier-side of the platform can charge to the consumers through competing distribution sources.7 Given the nuances that distinguish PMFNs from MFNs, economists have added to the general MFN research with literature on PMFNs investigating both the potential procompetitive and potential anticompetitive impacts of those PMFNs.8

A concern for antitrust litigators and regulators is the potential for PMFNs to reduce price and/or product competition. A PMFN imposed by one platform may restrict a seller’s/supplier’s ability to lower the price (or vary products) to buyers/consumers on competing platforms. Without being able to offer lower consumer prices (or variation in products), platforms may struggle to differentiate themselves from a dominant platform in such a way as to compete effectively and attract enough consumers to survive and become a successful platform. Reduction in competition could then lead to higher platform fees and consumer prices.9 A PMFN may further reduce competition by lowering incentives for potential entrants to join the marketplace at all,10 which may also result in more concentrated markets.11

These antitrust concerns have piqued interest in PMFN policies in both litigation and regulation. A notable example is the regulation of PMFNs in the hotel booking space by France, Italy, and Sweden in April 2015, which led to Booking.com and Expedia (the two largest online travel agency platforms) to restrict “wide” price parity clauses within the E.U.12 Later, France prohibited all price parity clauses in for French hotels in July 2015, and Germany prohibited all price parity clauses—wide and narrow—for Booking.com in December 2015.13 As a key example of PMFN litigation, in 2021, a class action was brought against Amazon and the “Big Five” book publishers accusing them of colluding to fix the price of ebooks at artificially high rates using MFN clauses.14 This case closely mirrored a 2011 case against Apple and the Big Five publishers, in which the Big Five settled and Apple lost at trial and was ordered to pay $450 million.15

Given past litigation and enforcement related to PMFNs and the general increased scrutiny in the Big Tech space, we expect that PMFNs will continue or increase in being an area of antitrust interest. Further, the litigation and enforcement, along with the existing literature, relating to the potential impacts of PMFNs highlight the importance of rigorous economic analysis and sound expert economic testimony to provide cases with clear conclusions on which side of the competitive scale the PMFN falls.

1 Legal Information Institute Website, Most Favored Nation, https://www.law.cornell.edu/wex/most_favored_nation (accessed 1/11/2024). (“Most favored nation refers to a status conferred by a clause in which a country promises that it will treat another country as well as it treats any other country that receives preferential treatment. Most favored nation clauses are frequently included in bilateral investment treaties.”)

2 Baker, Jonathan B. and Judith A. Chevalier (2013), “The Competitive Consequences of Most-Favored-Nation Provisions,” Antitrust 27(2): 20–26, at 20. (“Under an MFN, one party to a transaction promises to give the other party at least as favorable contractual terms as it gives any other counterparty.”)

3 Baker, Jonathan B. and Judith A. Chevalier (2013), “The Competitive Consequences of Most-Favored-Nation Provisions,” Antitrust 27(2): 20–26, at 20. (“Under an MFN, one party to a transaction promises to give the other party at least as favorable contractual terms as it gives any other counterparty.”)

4 Parker, Geoffrey G., Marshall W. Van Alstyne, and Sangeet Paul Choudary (2016), Platform Revolution, New York, NY: W. W. Norton & Company, at 5. (“A platform is a business based on enabling value-creating interactions between external producers and consumers.”)

Hovenkamp, Herbert J. (2020), “Antitrust and Platform Monopoly,” Yale Law Journal 130: 1952–2273, at 1957.

5 Baker, Jonathan B. and Fiona Scott Morton (2018), “Antitrust Enforcement Against Platform MFNs,“ Yale Law Journal 127(7): 2176–2202, at 2716, 2178. (“A platform MFN requires that providers refrain from offering their products or services at lower prices on other platforms. The platform is thus guaranteed that no other internet distributor will charge a lower final price, not because the focal platform has worked to ensure that it has the lowest cost, but rather because it has contracted for competitors’ prices to be no lower.”)

Boik, Andre, and Kenneth S. Corts (2016), “The Effects of Platform Most-Favored-Nation Clauses on Competition and Entry,” The Journal of Law and Economics 59(1): 105–134, at 105. (“In the context of sellers who sell their products through intermediary platforms, a platform most-favored-nation (PMFN) clause is a contractual restriction requiring that a particular seller will not sell at a lower price through a platform other than the one with which it has the PMFN agreement.”)

6 Baker, Jonathan B. and Fiona Scott Morton (2018), “Antitrust Enforcement Against Platform MFNs,“ Yale Law Journal 127(7): 2176–2202, at 2178. (“Platform MFNs are labeled ’wide’ if they constrain the price on all other platforms, including the provider’s own website (if any). In contrast, platform MFNs are considered ’narrow’ if they prevent the provider from setting a lower price on its own website, while leaving prices on other platforms unrestricted.”)

7 Boik, Andre, and Kenneth S. Corts (2016), “The Effects of Platform Most-Favored-Nation Clauses on Competition and Entry,” The Journal of Law and Economics 59(1): 105–134, at 105, 108. (“In the context of sellers who sell their products through intermediary platforms, a platform most-favored-nation (PMFN) clause is a contractual restriction requiring that a particular seller will not sell at a lower price through a platform other than the one with which it has the PMFN agreement.”; “In a traditional MFN policy, one or more sellers commit to one or more buyers not to sell to other buyers at a lower price. . . . Note that a platform setting is quite different in several ways. Most notably, a PMFN clause is an agreement between a seller and a platform about prices charged by the seller to a third party–the buyer.”)

8 See, for example:

Johnson, Justin P. (2017), “The Agency Model and MFN Clauses,” The Review of Economic Studies, 84(300): 1151–1185, at 1151.

Boik, Andre and Kenneth S. Corts (2016), “The Effects of Most-Favored-Nation Clauses on Competition and Entry,” The Journal of Law and Economics 59(1): 105–134, at 112.

Wang, Chengsi and Julian Wright (2020), “Search Platforms: Showrooming and Price Parity Clauses,” RAND Journal of Economics, 51(1): 32–58, at 32.

9 Boik, Andre and Kenneth S. Corts (2016), “The Effects of Platform Most-Favored-Nation Clauses on Competition and Entry,” Journal of Law and Economics 59(1): 105–134, at 128. (“We show that PMFN agreements tend to raise fees charged by platforms and prices charged by sellers[.]”)

10 Boik, Andre and Kenneth S. Corts (2016), “The Effects of Platform Most-Favored-Nation Clauses on Competition and Entry,” Journal of Law and Economics 59(1): 105–134, at 128. (“We also show that the adoption of a PMFN agreement by an incumbent platform can discourage entry by another platform if it is sufficiently downward differentiated[.]”)

11 See for example:

Rogerson, William P. and Howard Shelanski (2020), “Antitrust Enforcement, Regulation, and Digital Platforms,” University of Pennsylvania Law Review 168: 1911–1940, at 1938. (“The second type of behavior is the use of most favored nation clauses (MFN) that make it more difficult for potential competitors to challenge the dominant provider. For example, in the case of platforms that help businesses reach customers (such as a travel site that lists hotel accommodations), a MFN by a dominant platform that prohibits businesses from offering better terms on other platforms can limit the ability of potential competitors to challenge the incumbent.”)

Ezrachi, Ariel (2015), “The Competitive Effects of Parity Clauses on Online Commerce,” European Competition Journal, 11(2–3): 488–519, at 501, 519. (“The anticompetitive effects described above have been central to the analysis of wide MFNs worldwide. Indeed, a review of the main decisions by competition agencies reveals a consensus as to the possible harmful effects which wide MFNs combined with an agency model may generate. The most publicised case which involved wide MFNs, and was pursued on both sides of the Atlantic, concerned Apple’s use of wide parity in its iBooks Store.” Price parity clauses “may lead to a restriction of competition through excessive intermediation and price uniformity and they may also limit low cost entry.”)

12 Ennis, Sean, Marc Ivaldi, and Vincente Lagos (2022), “Price Parity Clauses for Hotel Room Booking: Empirical Evidence from Regulatory Change,” Toulouse School of Economics Working Paper, available at: https://www.tse-fr.eu/sites/default/files/TSE/documents/doc/wp/2020/wp_tse_1106.pdf, at 7–8.

13 Ennis, Sean, Marc Ivaldi, and Vincente Lagos (2022), “Price Parity Clauses for Hotel Room Booking: Empirical Evidence from Regulatory Change,” Toulouse School of Economics Working Paper, available at: https://www.tse-fr.eu/sites/default/files/TSE/documents/doc/wp/2020/wp_tse_1106.pdf, at 7–8.

14 The Guardian, “Amazon.com and ‘Big Five’ Publishers Accused of eBook Price-Fixing,” 1/15/2021, https://www.theguardian.com/books/2021/jan/15/amazoncom-and-big-five-publishers-accused-of-ebook-price-fixing.

15 The Guardian, “Amazon.com and ‘Big Five’ Publishers Accused of eBook Price-Fixing,” 1/15/2021, https://www.theguardian.com/books/2021/jan/15/amazoncom-and-big-five-publishers-accused-of-ebook-price-fixing.

In Antitrust analysis in the United States, the Small but Significant Non-Transitory Increase in Price (“SSNIP”) test is often a key component of market definition analysis, whether performed quantitatively or qualitatively. In this analysis, an entity is hypothesized to be a monopolist with respect to a product or set of products that are under consideration to be a relevant market. The analysis asks whether this hypothetical monopolist could profitably impose and sustain a small, but significant non-transitory increase in price (often defined to be a 5% price increase). If the answer is “yes,” the set of products under consideration is a relevant market. If the answer is “no,” the set of products under consideration is expanded successively until the SSNIP can be profitably sustained. The SSNIP test captures economic considerations of substitutability and cross-elasticity of demand by considering potential substitution among competing products and may therefore be used to define both the relevant product and geographic dimensions of the relevant market.

While the SSNIP test has dominated antitrust analyses in the United States, other tests of market definition and market power have seen increasing use in the European Union. One example of an alternative to an SSNIP is the Small but Significant Non-Transitory Decrease in Quality (“SSNDQ”) test. This test is similar to the SSNIP test in that it considers a hypothetical monopolist of a set of products or services but, instead of imposing a hypothetical increase in prices of this product or service, it analyses possible substitution effects following a decrease in the quality of these products or services. Like the SSNIP test, the SSNDQ test can be used to draw the boundaries of a relevant antitrust market and understand the potential for market power.

Notably, in zero-price markets, the European Union has recommended the use of an SSNDQ as an alternative to an SSNIP. While pricing power has historically been a hallmark of market power and may be readily observed in traditional industries, with the rise of the digital economy, many of the world’s largest firms now operate in the zero-price economy. For example, social media companies like Meta, search engines like Google, and digital apps like Yelp are “free” to users, in that users trade their data to the company and its advertisers to use the product or service for $0. Because of this, defining a market using the traditional SSNIP test, or evaluating market power through a pricing analysis, imposes both empirical and even conceptual challenges. Alternatively, using an SSNDQ test allows the fact finder to maintain the zero-price nature of a basket of potentially competitive goods while still considering how consumers may substitute away from certain products given a change in a product’s value – where value contains elements of both pricing and quality.

Indeed, there is some evidence that a greater move towards quality considerations in market definition may be on the horizon. For example, in the DOJ’s recent case against Google related to its monopolization of general search services, Judge Amit Metha, in his opinion, cited evidence of Google’s ability to decrease the quality of its search engine as evidence of its monopoly power in the market for general search services. However, the potential import of an SSNDQ test to the United States would likely bring both additional opportunities and additional considerations for market definition analyses going forward.

In February 2023, Novant agreed to purchase Lake Norman Regional Medical Center (LNR) and Davis Regional Psychiatric Hospital (Davis) from CHS. Novant is one of the largest health systems in NC, operating multiple facilities across the state. On the other hand, CHS is a national for-profit health system, and the LNR and Davis facilities represent CHS’s most important assets in NC. CHS wanted to sell LNR because the facility needed substantial capital investments, which CHS was not willing to make. The Davis facility was a former acute care hospital that, due to its poor performance and investment needs, was repurposed as a psychiatric facility. The transaction between Novant and CHS aimed to improve Novant’s competitive edge relative to Atrium Health (Atrium), NC’s largest health system.

The FTC decided to challenge the transaction in January 2024, initiating an administrative procedure and subsequently filing a complaint to block the deal in the US District Court for the Western District of NC. The FTC argued that LNR and Novant’s nearby hospital are head-to-head competitors and the main hospital options in the Eastern Lake Norman area, the relevant geographic market for the transaction. As such, LNR exerts competitive pressure on Novant, limiting Novant’s ability to increase prices, the FTC argued.

In June 2024, the district court ruled in favor of CHS and Novant by rejecting FTC’s preliminary injunction request. However, the FTC appealed at the US Court of Appeals for the 4th Circuit, which, in a divided decision, reverted the district court’s decision and granted the request to enjoin the CHS-Novant deal. Following this setback, the parties abandoned the deal. The appeals court’s ruling does not explain why the district court decision had to be reverted, with the dissenting judge explicitly agreeing with the district court that the injunction is not in the best public interest.

Three features make this case of particular interest for antitrust economic analysis. First, one of the parties, CHS, had decided to exit the market and stopped actively competing. Second, the transaction seemed to have meaningful potential pro-competitive effects. Third, the buyer, Novant, committed not to increase prices for three years after the transaction.

Whether you are an economist, attorney, antitrust enthusiast, or just curious about Secretariat, we are glad you found us. This publication showcases insights from leading economists about recent developments in law and economics that may significantly impact the field of antitrust. This issue explores recent topics in the economics of antitrust analysis, with implications for merger analysis, market definition, and anticompetitive conduct.

In the first article of this issue, Dr. Pablo Varas covers important economic lessons from the abandoned deal between Novant Health and Community Hospital Systems in North Carolina. This article highlights aspects of the deal that differed from more typical healthcare acquisitions and explores how they may impact proposed mergers going forward.