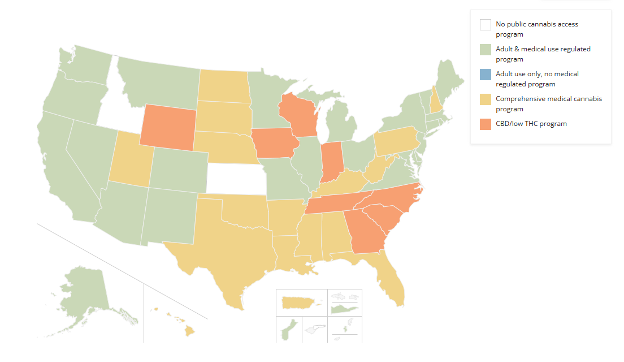

Cannabis legalization is expanding across U.S. states, and the cannabis sector has emerged as a significant regulated industry with growing competition policy implications. The state of competition in the U.S. cannabis industry is uniquely complex due to the interplay between federal prohibition[i] and state-level legalization.[ii] In states that have legalized medical or recreational use of cannabis, the sector has expanded rapidly[iii]. This has created a patchwork of local markets with barriers to interstate commerce, that to some extent insulates regional operators from the broader competitive pressures. Figure 1 illustrates how state regulations differ across the country. Although the FTC and DOJ retain jurisdiction to apply federal competition law, the continued federal illegality of cannabis under the Controlled Substances Act has created institutional uncertainty regarding the scope and propriety of federal engagement. In practice, most competition disputes in the sector have been addressed by state attorneys general and private litigants.

Figure 1: State Regulated Cannabis Programs

Source: National Conference of State Legislatures. “State Medical Cannabis Laws.” NCSL, 2024.

These diverse state-level policies have, to some extent, shaped the structure of the modern U.S. cannabis industry,[iv] which is best understood as a vertically structured supply chain rather than a single unified market. At the upstream level are cultivators that grow cannabis plants and manufacturers that process raw cannabis into derivative products such as concentrates, edibles, tinctures, and infused goods. Within this level, firms differentiate themselves through branding, potency, and product format.[v] Downstream are distributors (in some states) and retail dispensaries that sell directly to consumers. Because regulation varies by jurisdiction, some firms operate across multiple stages while others are restricted to a single level.

Potential antitrust issues can arise at every level of the U.S. cannabis industry under the current market structure. Horizontal concerns may occur among growers, manufacturers, or retailers competing within the same tier.[vi] In addition, vertical relationships—such as supply agreements, exclusivity provisions, and integration mandates—create potential vertical restraint issues linking different levels of the industry. Regulatory features including licensing caps and vertical integration requirements can amplify these concerns by limiting entry and altering competitive incentives.[vii],[viii]

Regulators and policymakers have increasingly expressed concern regarding state cannabis regulatory frameworks,[ix] in particular to the increased consolidation among MSOs.[x] Vertical integration requirements in some states—where licensees must control multiple stages of the supply chain—can limit competition by favoring larger, better-capitalized companies.[xi] Additionally, licensing caps and residency requirements often restrict the entry of new competitors, which can lead to oligopolistic market structures. Courts have increasingly entertained constitutional and competition-related challenges to state protectionist rules, such as residency requirements for cannabis licenses.[xii] These dynamics may unintentionally foster anti-competitive environments that could harm consumers and small businesses.

One particularly important issue that has thus far remained in the domain of state and private antitrust action is geographic market definition as it relates to retail cannabis sales. Because cannabis cannot legally cross state lines, one might assume relevant markets should be established within state borders.[xiii] However, antitrust analysis focuses on substitution patterns and consumer behavior rather than regulatory borders. It assesses how far consumers are willing to travel in response to a small but significant non-transitory price increase.[xiv] In many retail industries, including grocery stores and retail gasoline, enforcement agencies routinely define highly localized markets because consumers respond to price changes within short travel distances.[xv] Cannabis retail competition appears to follow a similar pattern. In a recent matter analyzing dispensary competition in Washington, D.C., I found localized submarkets within the District and measurable cross-border competition between dispensaries near the D.C.–Maryland boundary despite differing regulatory regimes. These findings suggest local competitive constraints may be more economically meaningful than jurisdictional boundaries.[xvi],[xvii]

In the meantime, the cannabis industry continues to operate in an uncertain regulatory landscape, where antitrust enforcement is highly fragmented. Consequently, there is considerable opportunity for state AGs and private parties to play key roles in shaping the industry in their localities. In this environment, any professional providing economic or legal analysis in cannabis-related antitrust matters must combine deep knowledge of competition principles with a practical understanding of the industry’s shifting regulatory framework.

[i] Cannabis remains a Schedule I substance under the Controlled Substances Act, preventing the federal government from formally regulating the market as it would other industries. While the DOJ has posted a proposal to transfer marijuana from schedule I of the Controlled Substances Act to schedule III in May 2024 (see Schedules of Controlled Substances: Rescheduling of Marijuana,89 FR 44597, May 21, 2024), followed by a reviewed proposal in August 2024 (see Schedules of Controlled Substances: Rescheduling of Marijuana, 89 FR 70148, August 29, 2024). On December 18, 2025, President Trump issued an executive order directing the Attorney General to take all necessary steps to expeditiously move marijuana from Schedule I to Schedule III under the Controlled Substances Act (CSA) – while the executive order does not reclassify marijuana as a Schedule III drug, the administration is signaling its support for the move. Ultimately, the United States is still navigating the administrative and legal mechanics of potentially rescheduling.

[ii] For a historical view of this process, see, for example, Congressional Research Service. The Evolution of Marijuana as a Controlled Substance and the Federal–State Policy Gap. Congressional Research Service, 2023. https://crsreports.congress.gov; Hudak, John. Marijuana: A Short History. Brookings Institution Press, 2016.

[iii] For a comprehensive and updated list of state cannabis regulations, see Marijuana Legality by State.” DISA Global Solutions, www.disa.com/marijuana-legality-by-state/; see also State Cannabis Legislation Database.” National Conference of State Legislatures, www.ncsl.org/health/state-cannabis-legislation-database.

[iv] For an analysis across multiple types of cannabis regulation in states and potential aspects that may influence their structure, see Wang, Lucy Xiaolu, and Nicholas J. Wilson. “US State approaches to cannabis licensing.” International Journal of Drug Policy 106 (2022): 103755.

[v] Donnan, Jennifer, et al. “Characteristics that influence purchase choice for cannabis products: a systematic review.” Journal of cannabis research 4.1 (2022): 9 conduct a systematic review of characteristics impacting final consumer choice of cannabis products, and show that several aspects are taken under consideration, indicating an environment of competition of imperfect substitutes.

[vii] Smart, Rosalie, and Rosalie Liccardo Pacula. “Early Evidence of the Impact of Cannabis Legalization on Cannabis Use.” The Economic Journal, vol. 129, no. 622, 2019.

[viii] For academic analyses of cannabis license dynamics and competition in Washington state, see Hollenbeck, Brett, and Kosuke Uetake. “Taxation and market power in the legal marijuana industry.” The RAND Journal of Economics 52.3 (2021): 559-595; Thomas, Danna. “License quotas and the inefficient regulation of sin goods: Evidence from the washington recreational marijuana market.” Available at SSRN 3312960 (2019).

[ix] The FTC has reviewed large multi-state operator acquisitions — including the proposed Cresco Labs/Columbia Care transaction (see, for example, “Cresco Labs, Columbia Care Mutually Terminate $2 Bln Merger.” Reuters, 31 July 2023, www.reuters.com/markets/deals/cresco-labs-columbia-care-mutually-terminate-2-bln-merger-2023-07-31/). New York’s cannabis regulator has expressly justified ownership caps and vertical separation requirements as necessary to prevent excessive market concentration and dominance by large, well-capitalized operators (see About the Office of Cannabis Management.” New York State Office of Cannabis Management, cannabis.ny.gov/about-0; NY Cannabis Advisory Board Suggests Cap on Adult-Use Retail Licenses.” MJBizDaily, mjbizdaily.com/news/ny-cannabis-advisory-board-suggests-cap-on-adult-use-retail-licenses/399363/). Massachusetts policymakers and oversight bodies have explicitly expressed concern that the state’s cannabis market has structurally favored larger, often out-of-state operators at the expense of local and social equity businesses, reflecting broader worries about market concentration and barriers to competition (“Senate Acts to Reform Cannabis Industry Oversight, Licensure.” Massachusetts Legislature, malegislature.gov/PressRoom/Detail?pressReleaseId=296). California, despite being often referred to as a counterexample for being a large market, regulators still acknowledge local concentration and foreclosure risks (see, for example, California Cannabis Market Outlook at https://cdn.cannabis.ca.gov/wp-content/uploads/sites/2/2025/03/California-Cannabis-Market-Outlook-FNL.pdf).

[x]See “Top 5 Largest Multi-State Cannabis Companies in the US (2025).” CannStrategy, https://www.cannstrategy.com/post/top-5-largest-multi-state-cannabis-companies-in-the-us-2025

[xi] There is substantial variation in the vertical integration regulation across states, ranging from states that forbid vertical integration (e.g., Washington state – RCW § 69.50.328(2): “No licensed marijuana retailer may also be a licensed marijuana producer or processor”) to states that require it (e.g., Florida Statutes § 381.986(8)(e): “A licensed medical marijuana treatment center shall cultivate, process, transport, and dispense marijuana for medical use.”)

[xii]See, for example, Northeast Patients Group v. United Cannabis Patients & Caregivers of Maine, 45 F.4th 542 (1st Cir. 2022).

[xiii] It is important to note that several states have already passed regulation which should allow and regulate interstate commerce for when federal restriction is lifted: Oregon’s State Senate Bill 582 from 2019 would permit the state to enter into agreements to export marijuana to other states; Washington SB 5069 from 2023 states “Effective Date: The bill takes effect on the earlier of the date on which federal law is amended to allow for the interstate transfer of cannabis between authorized cannabis-related businesses or the U.S. Department of Justice issues an opinion or memorandum allowing or tolerating the interstate transfer of cannabis between authorized cannabis-related businesses”, and California Senate Bill 1326 from 2022 also states that it “shall not take effect unless one of the following occurs: (1) Federal law is amended to allow for the interstate transfer of cannabis or cannabis products between authorized commercial cannabis businesses; (2) Federal law is enacted that specifically prohibits the expenditure of federal funds to prevent the interstate transfer of cannabis or cannabis products between authorized commercial cannabis businesses; (3) The United States Department of Justice issues an opinion or memorandum allowing or tolerating the interstate transfer of cannabis or cannabis products between authorized commercial cannabis businesses; (4) The Attorney General issues a written opinion, through the process established pursuant to Section 12519 of the Government Code, that state law authorization, under an agreement pursuant to this chapter, for medicinal or adult-use commercial cannabis activity, or both, between foreign licensees and state licensees will not result in significant legal risk to the State of California under the federal Controlled Substances Act, based on review of applicable law, including federal judicial decisions and administrative actions.”

[xiv]See, for example, Robert Pitofsky, New Definitions of Relevant Market and the Assault on Antitrust, 90 COLUMBIA LAW REVIEW 7, 1805 (1990), p. 1806:“‘Definition of relevant market’ is an effort to describe the array of firms that currently produces or potentially will produce products that are sufficiently close substitutes to take business away from any firm or group of firms that attempts to exercise market power.”

[xv]See, for example, United States v. H&R Block, Inc., 833 F. Supp. 2d 36 (D.D.C. 2011); United States v. Bazaarvoice, Inc., 2014 WL 203966 (N.D. Cal. 2014); United States v. Sunoco, Inc., Competitive Impact Statement, U.S. Department of Justice, 2018. See also Federal Trade Commission, “Analysis of Agreement Containing Consent Orders to Aid Public Comment”, In the Matter of Dollar Tree, Inc. and Family Dollar Stores, Inc. File No. 141-0207, § III. Competition in the Relevant Markets, (2015).

[xvi] Robert Martin, et al. v. Sequential LLC, d/b/a Green Theory, et al., Case No. 2024-CAB-006014.

[xvii] Retail dispensaries in some jurisdictions also accept out-of-state medical cards, which may further facilitate cross-border demand substitution.

The current conflict in the Middle East has been as disruptive commercially as it has been geopolitically. Many businesses operating in the region are suffering from a combination of sharp demand declines, blocked routes to market, surging input costs, and physical damage to assets.

For the third consecutive year, Secretariat has been ranked No. 1 in the Global Arbitration Review (GAR) Expert Witness Firms’ Power Index 2026, unveiled March 26 at the GAR Awards during Paris Arbitration Week. For the third consecutive year, Secretariat has been ranked No. 1 in the Global Arbitration Review (GAR) Expert Witness Firms’ Power Index 2026, unveiled March 26 at the GAR Awards during Paris Arbitration Week.

Human factors experts play a critical role in infant formula and nutrition‑product litigation because the central questions in these cases—what caregivers perceive, understand, retain, and ultimately do—are questions about human capabilities and limitations, not merely regulatory compliance.